October 29, 2025

Download the full report

New tariffs, profit concerns, stretched valuations, and threats to Fed independence were just a few of the concerns that investors could hide behind during Q3. Despite those fears – maybe from a contrarian point of view because those fears existed and did not materialise – global equities posted broad-based and strong returns for the quarter. As we approach the final stretch of an eventful and profitable year, we thought it would be useful to structure this review in a manner to answer the most frequently asked questions from clients.

Is the market an AI driven bubble at risk of a major correction? In other words, is it time to take profits?

Given the strong rebound in global equities since April there is an increasing frequency of financial publications questioning whether the market is in an AI driven bubble at risk of a major correction.

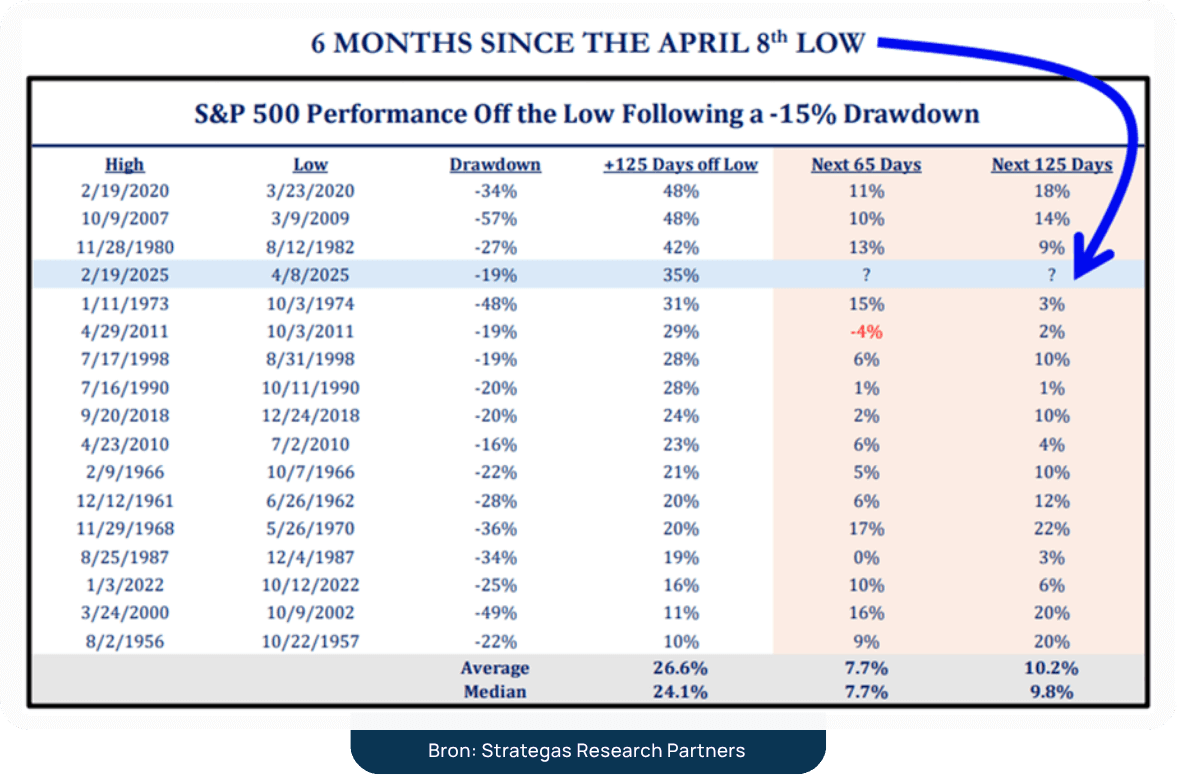

Historical evidence of previous market recoveries would suggest not. This is only the 10th time since 1929 that the US market has endured at least a -10% correction and is still up at least 10% at the end of Q3. The previous nine times, the S&P rose every time in Q4 by a median of 7.5% versus the historical average for Q4 returns of 2.7%.

The table below depicts previous drawdowns of at least -15% and then looks at the pattern of recovery following strong recoveries off that low.

The current recovery ranks fourth strongest over the last 70 years, and the last two columns on the right show the historical returns over the next three and six months – median returns of +7.7% and +9.8% respectively. Both significantly above average returns.

The simple message is that reversals of this strength tend to carry positive momentum.

Should investors abandon their European exposure given the strong momentum in US equities where the exposure to the AI theme is most concentrated?

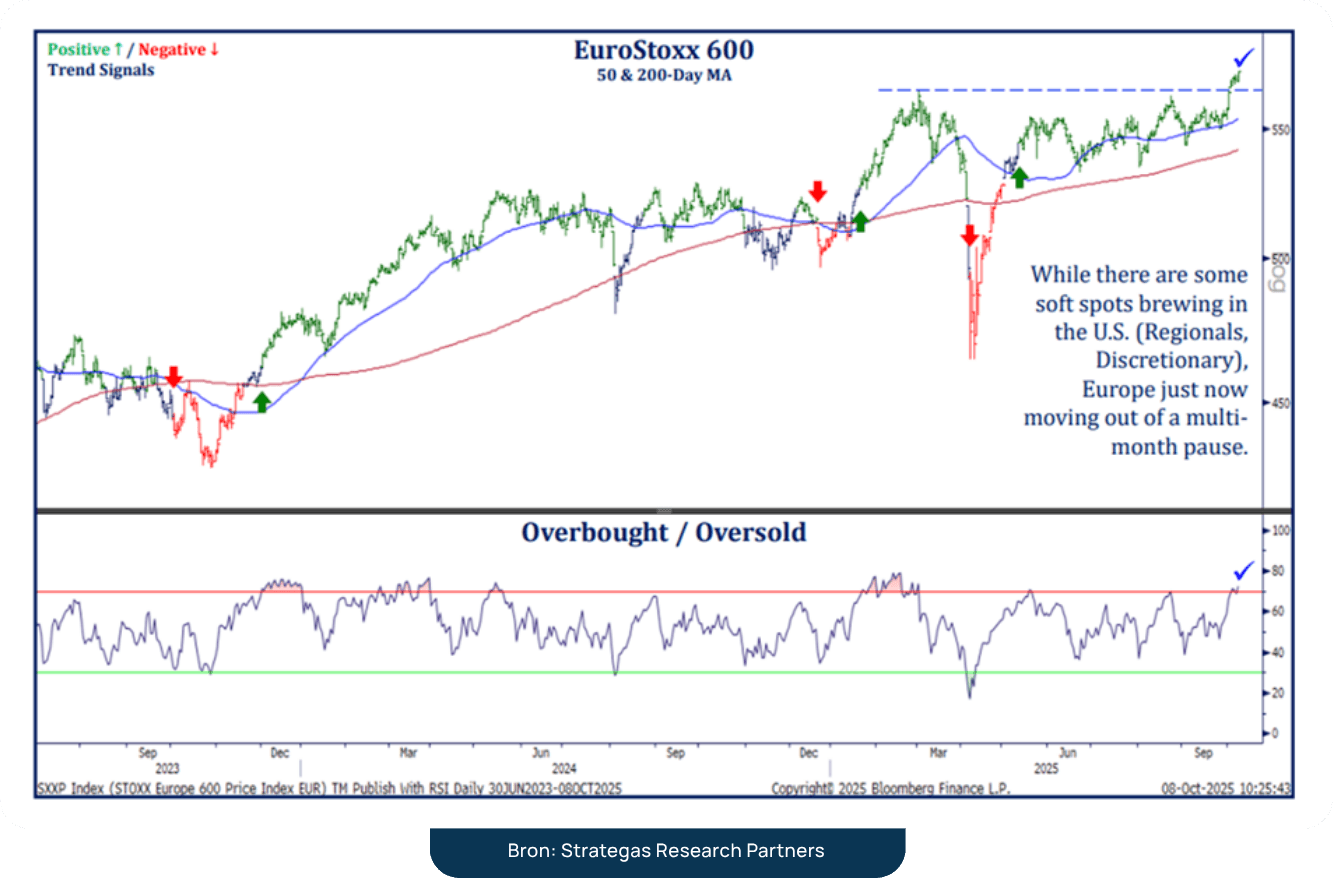

Europe ex-UK was the worst performing region in Q3, returning +2.6% and marking the second quarter in a row of underperformance relative to the US. Should investors abandon their European exposure given the strong momentum in US equities where the exposure to the AI theme is most concentrated? In our opinion simply NO. European companies have had to grapple with the dual headwinds of increased and uncertain tariffs and a significantly weaker US Dollar.

The result is that earnings estimates have come under pressure since ‘Liberation Day’ and the European indices have been stuck in a holding pattern for the last six months. However, as the chart below shows, we enter the historically strongest quarter of the year with

European equities just having significantly broken out to new highs. The major pan-European indices do not contain the valuation and concentration risk present in the US indices and offer an attractive and timely diversification benefit.

Equity valuations have risen further and are approaching levels in the US where the index has historically struggled to book further profits. Where then lie the investment opportunities in this context?

The majority of our investment ideas come from laborious company specific research and valuation where we hope to identify good businesses that are significantly mispriced.

Arcadis, the Dutch engineering company, is one such investment that we initiated in Q2 and added significantly to during the Q3.

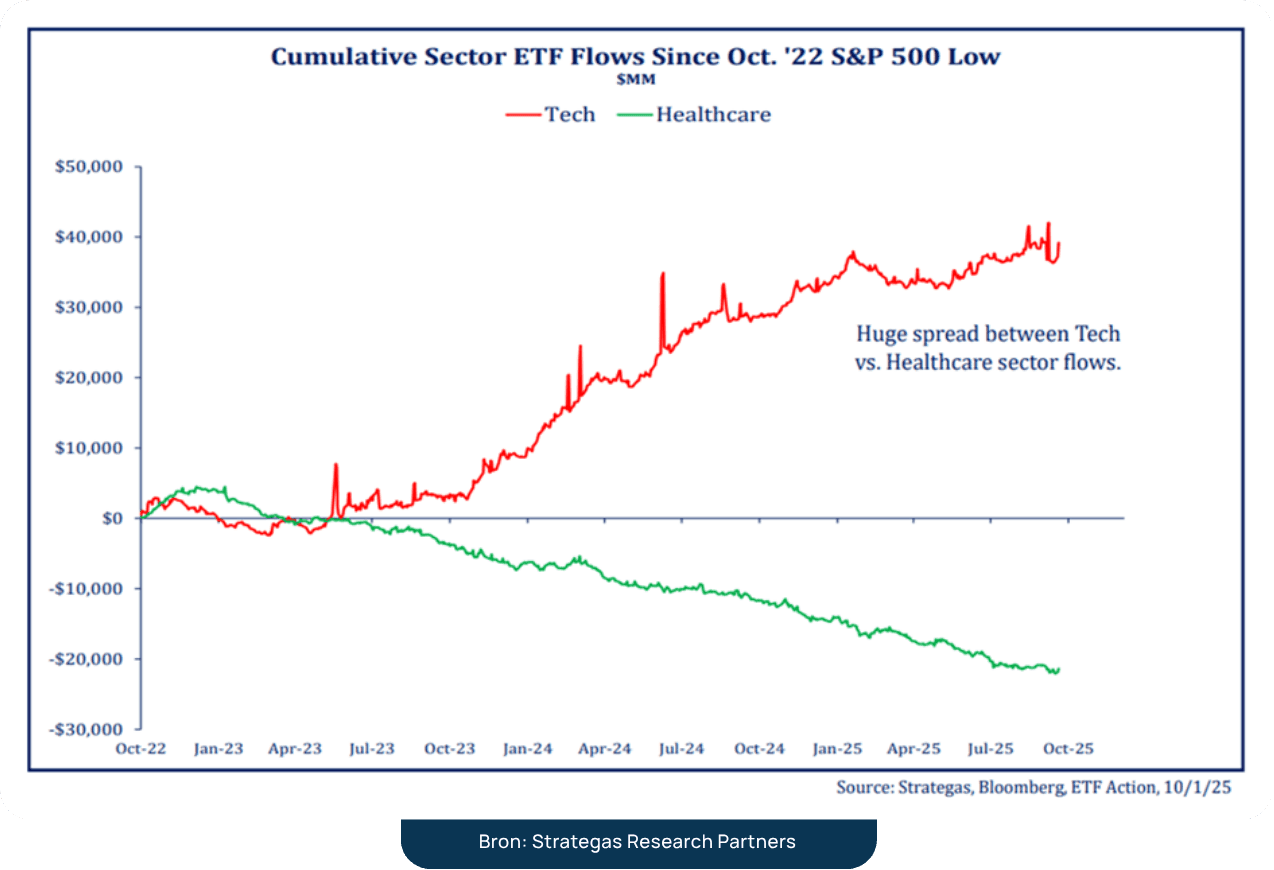

The herding tendency among investors can sometimes create a sector wide investment opportunity.

Global Healthcare stocks have endured a multi-year period of underperformance, partly due to relatively mediocre earnings growth but certainly exacerbated by the extreme investor flows into high momentum stocks/sectors and out of Healthcare (chart below).

Despite negative headline news, the European Healthcare sector has almost imperceptibly started to gather price momentum supported by multi-year low valuations and highly resilient business models. During the quarter, Healthcare surpassed Financials as our largest sector exposure as we added to names such as Novo Nordisk, AstraZeneca and Sanofi.

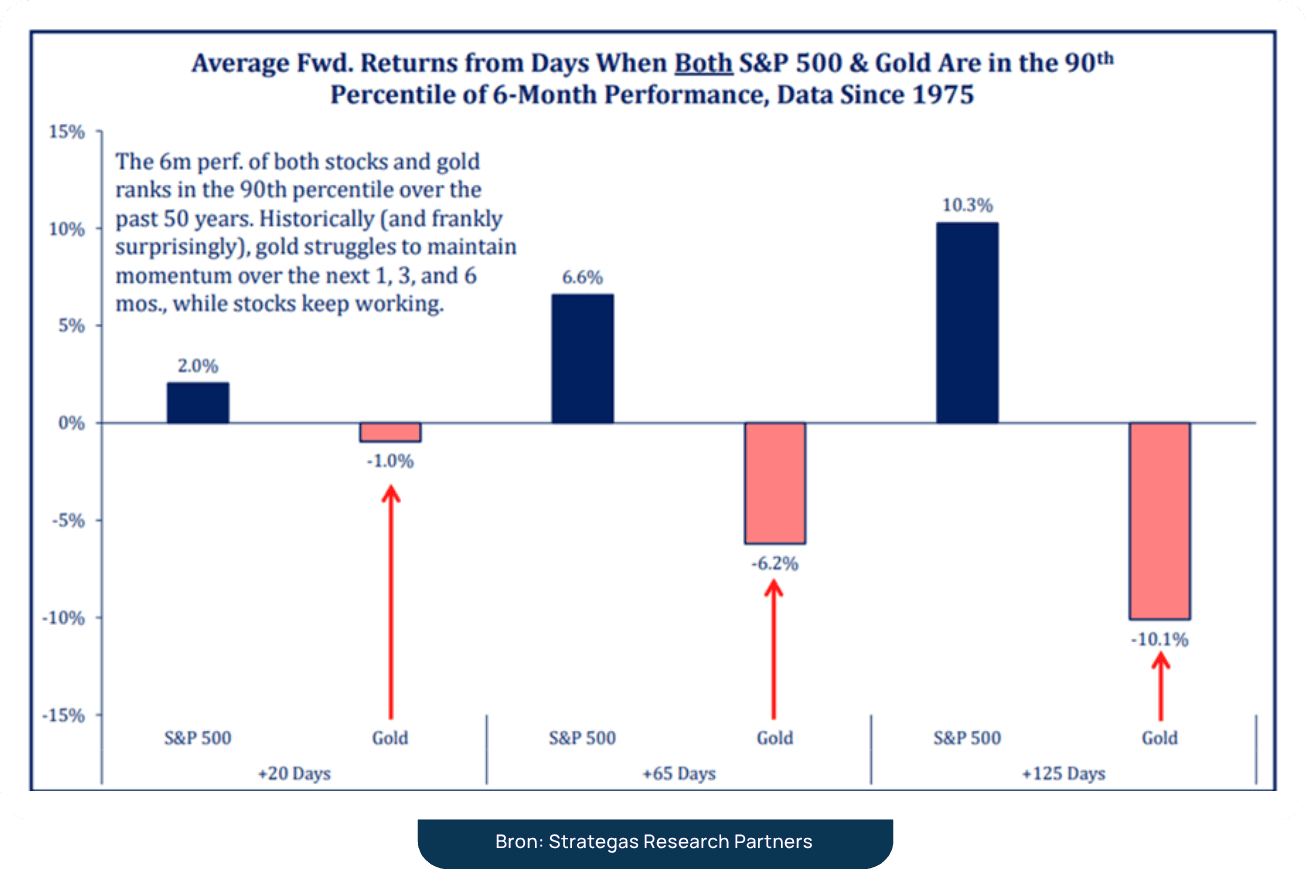

Why has Mpartners recently exited its gold exposure in the balanced accounts?

There is no shortage of narratives that have sprung up to justify the recent surge in the gold price – lack of fiscal discipline, loose monetary policy, inflation expectations, currency debasement, de-globalisation and the rise of economic nationalism.

We have been comfortable holders of gold for many years but the recent insatiable demand bears too close a similarity to previous frothy melt-ups that resulted at best in reduced near term return expectations.

Volume demand in gold EFTs and derivatives has recently hit all-time highs and other indicators of investor sentiment in gold indicate extreme optimism – all not positive indicators of short-term performance.

Interestingly, the chart below shows the forward returns based on the few historical occasions when both gold and stocks were posting strong six-month returns. Interestingly, it is stocks rather than the precious metal that historically has sustained the positive momentum.

Quite simply, given the current froth in the gold price we find more attractive investment opportunities in the equity universe.

In conclusion, we remain constructive on the market outlook as we enter what has historically been the strongest performance quarter of the year. There is no doubt that investor speculation is increasing, particulary in the most popular corners of the market that we have written about for some time.

That said, our portfolio remains an attractively valued (12x earnings) collection of strong businesses with solid balanced sheets where earnings momentum is increasing. We remain confident that our exposure to high quality companies selling at attractive valuations will allow for further gains during the remainder of the year.